Out of action

Out of action: means the life insured is solely as a result of sickness or injury, as diagnosed by a medical practitioner and on his/her advice and in our opinion is: — unable to attend or engage in his/her usual occupation; — not working in or performing any occupation, whether income generating or not; and — under the regular care of and following the advice of a medical practitioner, including recommended courses of treatment

Sickness or injury

Sickness: means an illness or disease that first manifests itself or is first suffered by the life insured after the cover commencement date or in the case of an increase to a benefit, after the commencement of the increase, and which is diagnosed by a medical practitioner. Injury: means an accidental bodily injury suffered by the life insured after the cover commencement date or in the case of an increase to a benefit or the addition of a benefit, after the commencement of the increase or benefit addition.

Income Protection Insurance

Income Protection helps you feel confident in your family’s financial security. It can help replace up to 75% of your income for a period of time if you find yourself out of action due to sickness or injury and need to maintain your lifestyle.

- Comprehensive cover up to 75% of your income up to $10,000 a month

- Flexibility to tailor your policy

- Quick and easy to apply

Get a quick quote

Or call 13 11 55

What is Income Protection Insurance?

If you experience illness or injury and you’re unable to work, income protection insurance provides regular, monthly payments for a specified time, so you can continue to pay your bills and living expenses. With Suncorp, you can receive up to 75% of your pre-tax income, up to $10,000/month.

Income protection features & benefits

Optional add-on

Accidental Injury Benefit

Designed to help you and your family with the financial strain of accidental injury, this will backdate the benefit payment to the date of your accidental injury, if it results in:

- Being totally out of action for the duration of the claim waiting period

- Remaining totally out of action beyond the end of the claim waiting period and eligible to receive a benefit or partial benefit

- The total benefits paid on any claim is up to the maximum claim benefit period nominated on your policy. The Accident Benefit Option is available if you take out Income Protect Plus Cover with a 14 or 28 day claim waiting period.

What's Not Included?

No benefit will be payable if the sickness or injury is caused directly or indirectly by:

Other exclusions may apply, including other specific exclusions agreed upon with you first and as listed in the policy schedule. Please see the PDS for further details.

How does income protection work?

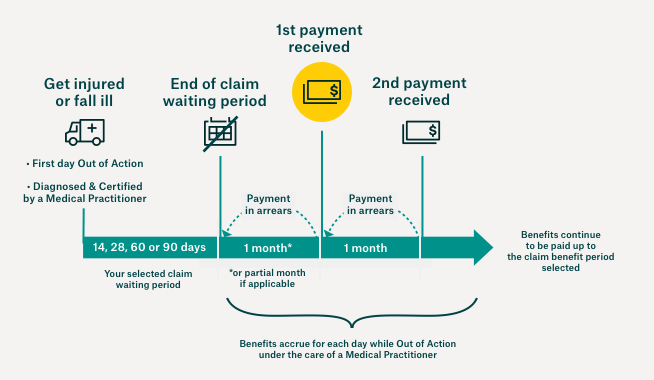

Income protection provides monthly payments if you’re unable to work due to illness or injury. You’ll serve certain waiting periods for income protection. You can choose a waiting period between 14 and 90 days, which means your benefit period will begin after that amount of time has passed.

You can choose a benefit period between 6 and 60 months.

Is income protection worth it?

Paying bills can be stressful if you’re struck by an unexpected illness or injury. Suncorp Income Protection Insurance provides peace of mind with regular monthly payments for a period of time to help keep your life on track if something goes wrong. There’s also built in financial assistance when returning to work and extra support for childcare to help protect your family.

Take the stress out of worrying about how you would cover your bills, get a quote.

Calculate your income protection cover

Help take control of your finances with Suncorp Income Protection, which you can tailor to suit your budget. How much you pay will depend on a few things, like your job, lifestyle and medical history, and the cover amount for bills and lifestyle costs. Get an income protection insurance quote online to see how you can personalise your policy.

Suncorp Life offers flexible cover so you can choose the right policy for you. For instance, if you have savings and you can afford a longer waiting period, you can select a 90-day waiting period and reduce your monthly premium.

Use the Income Protection Calculator to get an indication of how much cover you may need.

How to choose an income protection policy

Here are some things to consider when choosing income protection insurance.

Policy type: indemnity value policy or agreed value policy

Income protection comes in two policy types: indemnity value or agreed value.

- Indemnity value policy: this policy type insures you for a percentage of your salary at the time you make a claim. Suncorp Income Protection Insurance pays up to 75% of your monthly salary, based on the average of your last 12 months’ pay at the time of the claim. In some instances, indemnity value policies can be more cost-effective than agreed value policies.

- Agreed value policy: with this type of policy you receive a percentage of a set salary amount agreed upon with your insurer at the time of purchasing the policy. Although typically more expensive than indemnity value policies, agreed value policies may be useful for people with fluctuating incomes.

In April 2020, Australian life insurers stopped offering agreed value policies. Existing agreed value policies purchased before that time will remain valid. However, for new income protection policies only indemnity value policies are available.

Waiting period and benefit period

Waiting periods

- A waiting period is how long you’ll wait between making a successful claim and receiving your first payment.

- Suncorp offers a choice of 14, 28, 60 or 90 day waiting periods.

- Generally, longer waiting periods may assist with lower premiums

- After the waiting period if you’re still unable to work as a result of your sickness or injury you’ll become eligible for payments.

When selecting a waiting period you may want to consider your savings, sick leave or annual leave entitlements that could provide temporary financial support. You should consider the appropriateness of doing so based on your own personal needs and circumstances.

Benefit periods

- The benefit period is how long you’ll receive monthly payments for if you remain unable to work due to illness or injury.

- Suncorp Income Protection insurance policy benefit periods range from 6 months to 60 months – it’s your choice.

- Usually, longer benefit periods result in higher premiums.

How to apply for income protection

Are you:

If you answered yes to all these questions, then you’re eligible to apply for Suncorp Income Protection Insurance.

Why Suncorp Income Protection?

Australian residents

Australian residents aged 18 to 60 working 20 or more hours a week.

Quick and easy to apply

Apply online or over the phone with no medical exams required for Australian residents aged 18-60

Flexible for you

See how you can help tailor a policy to suit your needs, lifestyle and budget

Comprehensive cover

You can choose to insure up to 75% of your income, up to $10,000 a month with Income Protect Plus Cover

Extra support if you’re out of action

Receive a Recovery Support Benefit for up to two months if you’re confined to bed as a result of sickness or injury

Easy claims process

If you need to make a claim, a dedicated claims manager will make the process as stress-free as possible

We are helping Australians every day

With over one million dollars in accident, illness or injury claims paid every day

Frequently Asked Questions

Income protection insurance pays a monthly, ongoing benefit in accordance with your policy’s waiting period and benefit period, while life insurance pays a lump sum payment if you pass away or are diagnosed with a terminal illness. The main purpose of income protection is to insure your income, not your life. Also, unlike life insurance, the cost of income protection insurance is generally tax deductible when taken out outside of superannuation, meaning you can claim the cost of the policy each year at tax time.

According to the Australian Tax Office (ATO), you may be able claim the cost of the premiums that you pay for your income protection insurance against the loss of your income. You also need to include payments you receive through your income protection insurance as income.

If you are considering the tax implication of purchasing and receiving benefits under Suncorp Income Protection, it is important you seek independent, professional taxation advice.

Most superannuation funds offer a range of insurance policies including life, total and permanent disability (TPD) and income protection insurance for their members. When you purchase an income protection policy through your super fund, you’re limited to the options your fund has made available (e.g. their specific waiting periods, benefit periods and age restrictions). Policies purchased through a super fund are also generally not tax deductible against your income.

You can have both workers compensation and income protection, however, if you receive a workers compensation benefit, this may reduce your income protection insurance benefit. This is because Income protection is designed to help cover your loss of income, but if you’re already being compensated for the loss of that income from somewhere else, such as workers compensation, this will be factored in and generally your Income Protection benefit will be reduced accordingly.

Yes, you are eligible to apply for income protection insurance if you’re self-employed. In calculating your benefit amount, your business expenses are excluded from your pre-tax earnings to calculate your personal income. Note that income paid from rental income, investment income, other disability income policies, retirement plans or lump sum disability payments are some examples of income we would generally not consider to be part of earnings. Please refer to the Product Disclosure Statement (PDS) for further information.

Income protection insurance is designed to provide cover against illness or injury that affects your ability to earn an income. A redundancy is a difficult time, but it is not related to your personal health. Suncorp income protection Insurance won’t cover you if you’ve been made redundant or lose your job due to unforeseen circumstances.

Our claims specialists will help you understand the claims process, explain what to expect for the assessment of your claim, and make the claim process as easy as possible for you. We require you to fill out a claim form and provide documentation in support of your benefit entitlement. Please contact us on 1300 618 255 as soon as you know you will be out of action for longer than your claim waiting period, to avoid delays in processing your claim.

When assessing your application, we consider various personal and lifestyle factors, including the sports and hazardous activities you engage in, and whether they are for recreation or performed professionally. Certain recreational sports and activities, such as soccer or football, may be covered without amendment or may require a higher premium rate (called a 'premium loading') to be charged. Alternatively, we might apply a longer waiting period on your policy for claims from injuries sustained while participating in that specific sport or activity. We will inform you of any loadings or amendments before you decide to purchase cover, and the impact these options have on your premium.

Suncorp Life’s Commitment to the Life Insurance Code of Practice

Suncorp Life Insurance policies are issued by TAL, who played a key role in creating the Life Insurance Code of Practice. Suncorp Life is committed to delivering the best possible customer service standards. Suncorp Life will continue to look for ways to raise the standards of customer service now and over the years to come. Read more.

At TAL, we are committed to supporting our customers who may be experiencing vulnerability or have unique needs. Contact us or see how we can help if you are experiencing financial hardship or domestic and family violence.

Suncorp Income Protection is here to help

Call the Suncorp Life Team

For help with a quote, contact the Suncorp Life team about Income Protection Insurance today.

^ The ‘up to 10% discount’ offer is only available to customers who take out a quote and new Suncorp Income Protection or Life Insurance policy between 1st of April and 31st of July 2025. All eligible customers will receive a 5% discount automatically applied to their Suncorp Income Protection or Life Insurance premium for the life of the policy. Where an eligible customer is also an existing Suncorp customer who holds any other Suncorp branded insurance policy/ies such as home or car insurance, the 5% discount on premiums for Income Protection or Life Insurance will be automatically applied in addition to the standard 5% Existing Customer discount offered on Income Protection or Life Insurance. The two discounts combined amount to a total of 10% off Income Protection or Life Insurance premiums for the life of the policy.

Sickness or injury

Sickness: means an illness or disease that first manifests itself or is first suffered by the life insured after the cover commencement date or in the case of an increase to a benefit, after the commencement of the increase, and which is diagnosed by a medical practitioner. Injury: means an accidental bodily injury suffered by the life insured after the cover commencement date or in the case of an increase to a benefit or the addition of a benefit, after the commencement of the increase or benefit addition.

Out of action

Out of action: means the life insured is solely as a result of sickness or injury, as diagnosed by a medical practitioner and on his/her advice and in our opinion is: — unable to attend or engage in his/her usual occupation; — not working in or performing any occupation, whether income generating or not; and — under the regular care of and following the advice of a medical practitioner, including recommended courses of treatment

Australian residents

Australian residents aged 18 to 60 working 20 or more hours a week.

Waiting period

Operating Hours

Quotes and sales: Mon-Fri 8am-7pm, Sat 9am-4pm (AEST)

Customer service: Mon-Fri 8am-6pm (AEST)

Claims: Mon-Fri 8am-5:30pm (AEST)